Getting started¶

We build a credit-risk premium system: a lender turns a borrower's credit

score (300–850) and debt-to-income ratio (dti, 0–50%) into a risk

premium (0–12 points) to add on top of its base interest rate.

1. Define linguistic variables¶

A Variable is a named universe plus named terms

(fuzzy sets). Generate terms automatically, or set them explicitly.

import fuzzytool as fz

# Explicit membership functions:

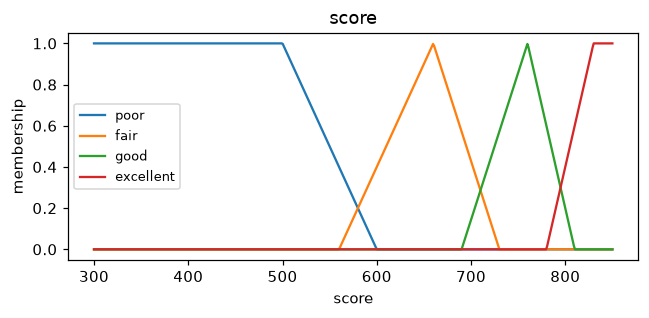

score = fz.Variable("score", (300, 850))

score["poor"] = fz.trap(300, 300, 500, 600)

score["fair"] = fz.tri(560, 660, 730)

score["good"] = fz.tri(690, 760, 810)

score["excellent"] = fz.trap(780, 830, 850, 850)

# Or auto-generated, evenly spaced terms:

dti = fz.Variable("dti", (0, 50), terms=["low", "moderate", "high"])

premium = fz.Variable("premium", (0, 12), terms=["low", "medium", "high"])

2. Write rules with operators¶

Indexing a variable with a term name gives a proposition you combine with

operators: & (AND, t-norm), | (OR, s-norm), ~ (NOT, complement).

sys = fz.Mamdani(defuzz="centroid")

sys.rule(score["poor"] | dti["high"], premium["high"])

sys.rule(score["fair"] & dti["moderate"], premium["medium"])

sys.rule(score["good"] | score["excellent"], premium["low"])

3. Run inference¶

The system is callable. Pass crisp inputs by variable name:

sys(score=800, dti=10) # strong borrower -> 2.45 pts (low premium)

sys(score=520, dti=42) # weak borrower -> 9.93 pts (high premium)

4. Visualize (optional)¶

import matplotlib.pyplot as plt

from fuzzytool import viz

viz.plot_variable(score)

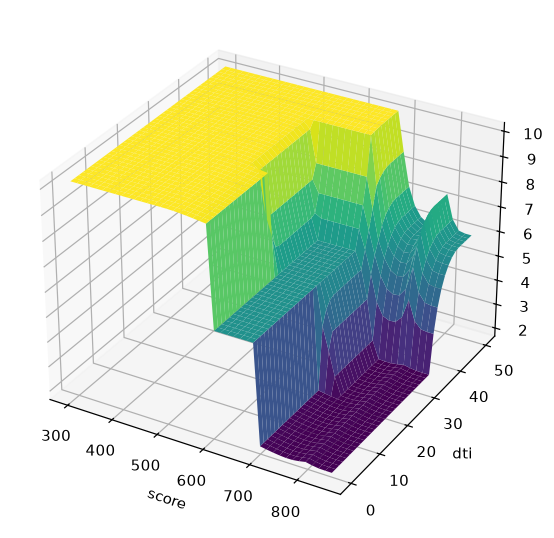

viz.control_surface(sys, score, dti)

plt.show()